Introduction

Generally, federal lands may not be taxed by state or local governments unless the governments are authorized to do so by Congress. Because local governments often are financed by property or sales taxes, this inability to tax the property values or products derived from the federal lands may affect local tax bases, sometimes significantly. If the federal government controls a significant share of a county's property, then the revenue-raising capacity of that county may be compromised. Instead of authorizing taxation, Congress usually has chosen to create various payment programs designed to compensate for lost tax revenue. These programs take various forms. Many pertain to the lands of a particular agency (e.g., the National Forest System [NFS] or the National Wildlife Refuge System [NWRS]).1

The most wide-ranging payment program is called Payments in Lieu of Taxes (PILT).2 It is administered by the Department of the Interior (DOI) and affects most acreage under federal ownership. Eligible lands consist of those in the National Park System (NPS), NFS, or Bureau of Land Management (BLM); certain lands in the NWRS if they are withdrawn from the public domain; lands dedicated to the use of federal water resources development projects; dredge disposal areas under the jurisdiction of the U.S. Army Corps of Engineers; lands located in the vicinity of Purgatory River Canyon and Piñon Canyon, Colorado, that were acquired after December 31, 1981, to expand the Fort Carson military reservation; lands on which are located semi-active or inactive Army installations used for mobilization and for reserve component training; and certain lands acquired by DOI or the Department of Agriculture under the Southern Nevada Public Land Management Act (P.L. 105-263). However, most military lands, lands under the Department of Energy (which have their own smaller payment program), lands of the National Aeronautics and Space Administration, and lands of the Department of Homeland Security are not eligible for payments under PILT.3 In FY2016, the PILT program covered 606.9 million acres, or about 94% of all federal land.

The Payments in Lieu of Taxes Act of 1976 (P.L. 94-565, as amended; 31 U.S.C. §§6901-6907) was passed at a time when U.S. policy was shifting from one of disposal of federal lands to one of retention. The policy meant the retained lands would no longer be expected to enter the local tax base at some later date. Because of that shift, Congress agreed with recommendations of a federal commission that if these federal lands were never to become part of the local tax base, some compensation should be offered to local governments (generally counties) to make up for the presence of nontaxable land within their jurisdictions.4 Moreover, there was a long-standing concern that some federal lands produced large revenues for local governments, whereas other federal lands produced little or none. Many Members, especially those from western states with a high percentage of federal lands, felt the imbalance needed to be addressed. The resulting law authorizes federal PILT payments to local governments. The payments may be used for any governmental purpose. In addition to the overall structure of the program, specific issues that have been included are payments for Indian or other categories of lands, and tax equivalency, especially for eligible urban lands.

Critics of PILT cite examples of what they view as its idiosyncrasies:

- A few counties that receive very large payments from other federal revenue-sharing programs (because of valuable timber, mining, recreation, and other land uses) also are authorized to receive a minimum payment ($0.37 per acre)5 from PILT.

- Although there is no distinction between acquired and public domain lands6 for other categories of eligible lands, acquired lands of the Fish and Wildlife Service (FWS) are not eligible for PILT. This provision works to the detriment of many counties in the East and Midwest, where nearly all FWS lands are acquired lands.

- Payments under the Secure Rural Schools (SRS) program7 require an offset in the following year's PILT payment for certain lands under the jurisdiction of the Forest Service (FS). However, if the eligible lands are under the jurisdiction of the BLM, there is no reduction in the next year's PILT payment.8

- Certain BLM lands (called the Oregon and California Grant Lands) receive payments that do not require an offset in the following year's PILT payment.9

- Some of the "units of general local government" (counties)10 that receive large payments have other substantial sources of revenue, and some of the counties that receive small payments are relatively poor.

- In some counties the PILT payment greatly exceeds the amount the county would receive if the land were taxed at fair market value, whereas in others it is much less.

Given such issues, and the complexity of federal land management policies, consensus on substantive change in the PILT law has been elusive.

|

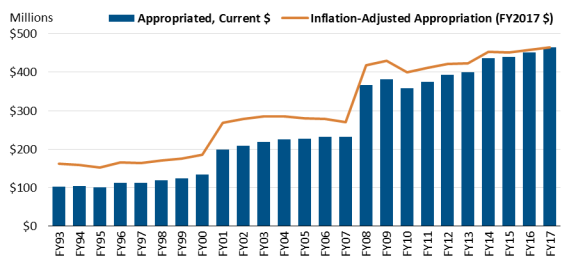

Figure 1. Total PILT Payments, FY1993-FY2017: Appropriations in Current and Inflation-Adjusted FY2017 Dollars |

|

|

Sources: Current dollars from the annual Payments in Lieu of Taxes: National Summary reports of the U.S. Department of the Interior's Office of Budget (hereinafter referred to as National Summary). Inflation adjustment is based on chain-type price index. The FY2017 GDP deflator price index was calculated using the average GDP deflator reported for the first three quarters of FY2017. Notes: For the same data in tabular format, see Table A-1. |

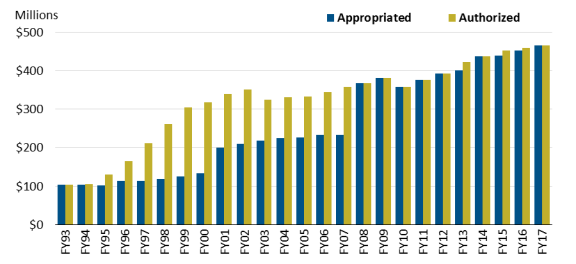

Many of the broader issues of federal compensation to counties that were addressed when PILT was created have reemerged over the years. One such issue is the appropriate payment level, which is complicated by erosion of the payments' purchasing power due to inflation. Until about 1994, the full amount authorized under the law's formula generally had been appropriated, with a few exceptions such as sequestration under the Gramm-Rudman-Hollings Act (Title II of P.L. 99-177). For many of PILT's first 15 years, counties held that payments effectively were declining because of inflation. A 1994 amendment (P.L. 103-397) was focused on increasing the total payments, building in inflation protection, and making certain additional categories of land eligible.11 The authorized payment level continued to be subject to annual appropriations. Figure 1 shows a major increase in both the actual and the inflation-adjusted dollars appropriated for PILT from FY1993 to FY2017.12 The increase in the authorization from the 1990s to the 2000s was not accompanied by a commensurate increase in appropriations. (See Figure 2.) The growing discrepancy between appropriations and the rising authorization levels led to even greater levels of frustration among many local governments and prompted intense interest among some Members in increasing appropriations.

|

Figure 2. Total PILT Payments, FY1993-FY2017: Authorized Amount and Appropriation |

|

|

Sources: Relevant annual National Summary reports. Note: For the same data in tabular format, see Table A-2. |

PILT Legislation and Funding

From the first PILT payment in FY1977 to FY2007, payments were provided through annual appropriations. Starting with the FY2008 payment, however, Congress enacted a series of changes to PILT payment funding, including approval of mandatory spending for the payments (see Table 1).

|

Fiscal Year |

Statute |

Funding Type |

Total Appropriated Amount (millions) |

% of Authorized Payment Amount |

|

FY2008-FY2012 |

Mandatory Spending |

Set in PILT formula |

100% |

|

|

FY2013 |

Mandatory Spending |

$400.2 |

94.9% |

|

|

FY2014 |

Mandatory Spending |

$436.9 |

100% |

|

|

FY2015 |

Discretionary Appropriation ($372.0) |

$439.5 |

97.3% |

|

|

Mandatory Spending ($33.0 and $34.5) |

||||

|

FY2016 |

Discretionary Appropriation |

$452.0 |

98.3% |

|

|

FY2017 |

Discretionary Appropriations |

$465.0 |

99.7% |

Source: Prepared by the Congressional Research Service (CRS).

Notes: Payment level reported in nominal dollars. FY2008-FY2013 payment levels are not shown here, but are available in the Appendix. In FY2013, the payment was subject to a sequestration reduction of 5.1%. In FY2015, one of the authorized mandatory spending payments was subject to a sequestration reduction of 6.8%.

PILT Legislation: The 110th to 113th Congresses

The 110th Congress enacted several changes in PILT funding. First, the Continuing Appropriations Act, 2009 (P.L. 110-329), provided funding at the FY2008 level ($228.9 million) through March 6, 2009. This figure would have constituted roughly 61% of the figure estimated for full payment of the FY2009 authorized level. Subsequently, the Emergency Economic Stabilization Act of 200813 provided for mandatory spending of the full authorized level for five years—FY2008-FY2012. (See Figure 2.)

Next, the Moving Ahead for Progress in the 21st Century Act (P.L. 112-141, §100111) extended mandatory spending for PILT to FY2013, without making any other changes to the law. Under the Budget Control Act (P.L. 112-25), PILT was categorized as a nonexempt, nondefense mandatory spending program. As such, it was subject to a 5.1% sequestration of the payments scheduled for FY2013, or $21.5 million from an authorized payment of $421.7 million.14

PILT Legislation: FY2014

For the FY2014 appropriations cycle, Congress faced two basic choices for FY2104 funding:

- continue the program through an appropriations act, which is constrained by procedural and statutory limits on discretionary spending; or

- provide funding through some measure other than an appropriations act, which would be treated as mandatory spending. With this choice, funding would be subject to certain budget rules that generally require such spending to be offset.

In either case, failure to find an offset would lead to certain procedural hurdles, such as points of order, although Congress sometimes sets aside or waives such points of order.15

The option for funding through an appropriations act was rejected when PILT funding was not included in the Consolidated Appropriations Act, 2014 (P.L. 113-76), although the Appropriations Committee members expressed support for the program in general.16 Instead, funding for the program was included in the Agricultural Act of 2014 (P.L. 113-79, §12312; H.Rept. 113-333; also called the 2014 farm bill), which extended mandatory spending for one year.17 The bill was a net reduction in mandatory spending and therefore offset the increase due to PILT payments. The PILT provision provided county governments with the full formula amount in summer 2014.

PILT Legislation: FY2015

The FY2015 payment was paid in June 2015.18 The Consolidated and Further Continuing Appropriations Act, 2015 (P.L. 113-235, §11), provided $372 million in discretionary spending. The Carl Levin and Howard P. "Buck" McKeon National Defense Authorization Act (NDAA; P.L. 113-291) included a provision (§3096) for $70 million in mandatory spending for PILT. Of this amount, $33 million was made available in FY2015; the remaining $37 million was to be made available after the start of FY2016 on October 1, 2015, leaving some doubt as to whether the amount should be considered a late payment for FY2015 or an early payment for FY2016. The Continuing Appropriations Act of 2016 (P.L. 114-53) included a provision (§138) clarifying that the October payment was to be considered a supplement for the FY2015 payment. Through sequestration, the additional $37 million was reduced by 6.8%, to $34.5 million. That amount bought the FY2015 total to $439.5 million, or 97.3% of the full formula amount.

PILT Legislation: FY2016 and FY2017

For FY2016, PILT payments were included in the Consolidated Appropriations Act, FY2016 (P.L. 114-113, Division G). The measure provided $452.0 million for PILT, an amount sufficient to provide 98.3% of the full payment of $459.5 million. For FY2017, PILT payments were included in the Consolidated Appropriations Act, FY2017 (P.L. 115-31), which provided $465.0 million for PILT, an amount sufficient to provide 99.7% of the full payment of $465.9 million. These payments were disbursed in June 2017.

How PILT Works: Five Steps to Calculate Payment

Calculating a particular county's PILT payment first requires answering several questions:

- How many acres of eligible lands are in the county?

- What is the population of the county?

- What were the previous year's payments, if any, for all of the eligible lands under the other payment programs of federal agencies?19

- Does the state have any laws requiring the payments from other federal agencies to be passed through to other local government entities, such as school districts, rather than staying with the county government?

- What was the increase in the Consumer Price Index for the 12 months ending the preceding June 30?

Each of these questions is discussed below, and the following section describes how the questions are used in the computation of each county's payment.

Step 1. How Many Acres of Eligible Lands Are There?

Nine categories of federal lands are identified in the law as eligible for PILT payments:20

- 1. Lands in the National Park System

- 2. Lands in the National Forest System

- 3. Lands administered by BLM

- 4. Lands in the National Wildlife Refuge System (NWRS) that are withdrawn from the public domain

- 5. Lands dedicated to the use of federal water resources development projects21

- 6. Dredge disposal areas under the jurisdiction of the U.S. Army Corps of Engineers

- 7. Lands located in the vicinity of Purgatory River Canyon and Piñon Canyon, Colorado, that were acquired after December 31, 1981, to expand the Fort Carson military reservation

- 8. Lands on which are located semi-active or inactive Army installations used for mobilization and for reserve component training

- 9. Certain lands acquired by DOI or the Department of Agriculture under the Southern Nevada Public Land Management Act (P.L. 105-263)

|

Section 6904/6905 Payments Two sections of the PILT law (31 U.S.C. §6904 and §6905) provide special payments for limited categories of land, for limited periods. These are described in the FY2016 National Summary (p. 12) as follows: Section 6904 of the Act authorizes payments for lands or interests therein, which were acquired after December 31, 1970, as additions to the National Park System or National Forest Wilderness Areas. To receive a payment, these lands must have been subject to local real property taxes within the five year period preceding acquisition by the Federal government. Payments under this section are made in addition to payments under Section 6902. They are based on one percent of the fair market value of the lands at the time of acquisition, but may not exceed the amount of real property taxes assessed and levied on the property during the last full fiscal year before the fiscal year in which [they were] acquired. Section 6904 payments for each acquisition are to be made annually for five years following acquisition, unless otherwise mandated by law.... Section 6905 of the Act authorizes payments for any lands or interests in land owned by the Government in the Redwood National Park or acquired in the Lake Tahoe Basin under the Act of December 23, 1980 (P.L. 96-586, 94 Stat. 3383). Section 6905 payments continue until the total amount paid equals 5 percent of the fair market value of the lands at the time of acquisition. However, the payment for each year cannot exceed the actual property taxes assessed and levied on the property during the last full fiscal year before the fiscal year in which the property was acquired by the Federal government. In FY2016, the Section 6904/6905 payments totaled $542,582, or 0.12% of the total program. California counties received the largest amount ($79,208). Eleven states, three territories, and the District of Columbia received no payments under these two sections in FY2016. The states were Arkansas, Illinois, Iowa, Kansas, Louisiana, Mississippi, Missouri, Nebraska, Oklahoma, Rhode Island, Wyoming, and the territories were Guam, Puerto Rico, and the Virgin Islands. The payments under Section 6904 cease five years after the acquired land is incorporated into a national park unit or a National Forest Wilderness Area. As a result, some counties experience a sudden drop in their PILT payment after five years. |

In addition, if any lands in the above categories were exempt from real estate taxes at the time they were acquired by the United States, those lands are not eligible for PILT, except in three circumstances:

- 1. Lands received by the state or county from a private party for donation to the federal government within eight years of the original donation

- 2. Lands acquired by the state or county in exchange for land that was eligible for PILT

- 3. Lands in Utah acquired by the United States if the lands were eligible for a payment in lieu of taxes program from the state of Utah

Only the nine categories of lands (plus the three exceptions) on this list are eligible for PILT payments; other federal lands—such as military bases, post offices, federal office buildings, and the like—are not eligible for payments under this statute. The exclusion of lands in the NWRS that are acquired is an interesting anomaly, and it may reflect nothing more than the fact that the House and Senate committees with jurisdiction over most federal lands did not have jurisdiction over the NWRS as a whole at the time P.L. 94-565 was enacted.22

Step 2. What Is the Population of the County?

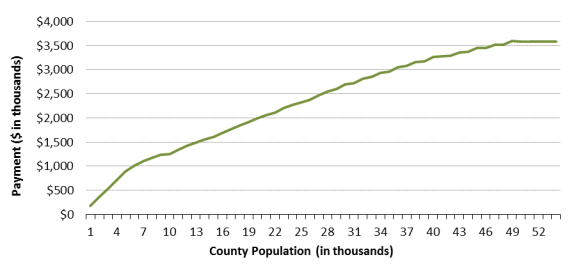

The law restricts the payment that a county may receive based on population by establishing a ceiling payment that rises with increasing population. (See Figure 3.) Counties are paid at a rate that varies with population; counties with low populations are eligible for payment totals at a higher rate per person and populous counties are paid less per person.23 For example, for FY2017, a county with a population of 1,000 people could not receive a PILT payment of more than $179.15 per person ($179,150 in total); a jurisdiction with a population of 30,000 could not receive a payment over $2.69 million (30,000 people × $89.61 per person). And no county can be credited with a population of more than 50,000, even if its actual population is many times larger. For example, in FY2017, at the authorized payment level of $71.67 per person, a county with a population of 1,000,000 could not receive a PILT payment over $3.58 million (50,000 people × $71.67 per person). Figure 3 shows the relationship between the population of a county and the maximum PILT payment.

Step 3. Are There Prior-Year Payments from Other Federal Agencies?

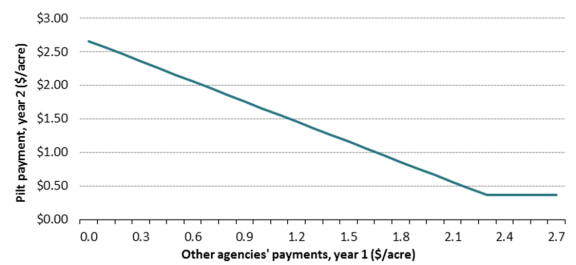

Federal land varies greatly in revenue production. Some lands have a large volume of timber sales or recreation concessions such as ski resorts, and others generate no revenue at all. Some federal lands have payment programs for state or local governments, and these payments may vary markedly from year to year. To even out the payments among counties and prevent grossly disparate payments, Congress provided that the previous year's payments on eligible federal lands from specific payment programs to counties would be subtracted from the PILT payment of the following year. So for a hypothetical county with three categories of eligible federal land, one paying the county $1,000, the second $2,000, and the third $3,000, then $6,000 would be subtracted from the following year's PILT payment. Most counties are paid under this offset provision, which is called the standard rate. In Figure 4, the standard rate is shown by the left, sloping portion of the line, indicating that as the sum of the payment rates from other agencies increases, the PILT payment rate declines on a dollar-for-dollar basis.

At the same time, Congress wanted to ensure that each county with eligible lands got some PILT payment, however small, even if the eligible lands produced substantial county payments from other agencies. If the county had payments from three federal payment programs of $1,000, $2,000, and $1 million, for instance, subtracting $1.003 million from a small PILT payment would produce a negative number—meaning no PILT payment to the county at all. In that case, a minimum rate applies, which does not deduct the other agencies' payments. In Figure 4, the flat portion to the right shows that, after the other agencies' payments reach a certain level (over $2.29 per acre in FY2017), the rate of the PILT payment remains fixed (at $0.37 per acre in FY2017).

The payments made in prior years that count against future PILT payments are specified in law.24 Any other payment programs beyond those specified would not affect later PILT payments. These specified payments are shown in Table A-3. Eligible lands under some agencies (e.g., National Park Service and Army Corps of Engineers) have no payment programs that affect later PILT payments.

Step 4. Does the State Have Pass-Through Laws?

Counties may receive payments above the calculated amount described above, depending on state law. Specifically, states may require that the payments from federal land agencies pass through the county government to some other entity (typically a local school district) rather than accrue to the county government itself. When counties in a pass-through state are paid under the formula that deducts their prior-year payments from other agencies (e.g., from the Refuge Revenue Sharing Fund [RRSF; 16 U.S.C. §715s] of FWS or the Forest Service [FS] Payments to States program [16 U.S.C. §500]),25 the amount paid to the other entity is not deducted from the county's PILT payments in the following year. According to DOI:

Only the amount of Federal land payments actually received by units of government in the prior fiscal year is deducted. If a unit receives a Federal land payment, but is required by State law to pass all or part of it to financially and politically independent school districts, or any other single or special purpose district, payments are considered to have not been received by the unit of local government and are not deducted from the Section 6902 payment.26

For example, if a state requires all counties to pass along some or all of their RRSF payments from FWS to the local school boards, the amount passed along is not deducted from the counties' PILT payments for the following year.27 Or if two counties of equal population in two states each received $2,000 under the FS Payments to States program, and State #1 pays that amount directly to the local school board but State #2 does not, then under this provision the PILT payment to the county in State #1 will not be reduced in the following year but that of the county in State #2 will drop by $2,000. State #1 will have increased the total revenue coming to the state and to each county by taking advantage of this feature.28

Consequently, the feature of PILT that apparently was intended to even out payments among counties (at least of equal population size) may not have that result if a state takes advantage of this pass-through feature.29 Each governor is required to report annually to the Secretary of the Interior with a statement of the amounts actually paid to each county government under the relevant federal payment laws.30 DOI also cross-checks each governor's report against the records of the payment programs of federal agencies.

In addition, there is a pass-through option for the PILT payment itself. A state may require that the PILT payment go to a smaller unit of government, contained within the county (typically a school district).31 In this case, one check is sent by the federal government to the state for distribution by the state to these smaller units of government. The distribution must occur within 30 days. To date, Wisconsin is the only state to have elected to pass through PILT payments.

Step 5. What Is This Year's Consumer Price Index?

A provision in the 1994 amendments to PILT adjusted the authorization levels for inflation. The standard and minimum rates, as well as the payment ceilings, are adjusted each year. The PILT statute requires that "the Secretary of the Interior shall adjust each dollar amount specified in subsections (b) and (c) to reflect changes in the Consumer Price Index published by the Bureau of Labor Statistics of the Department of Labor, for the 12 months ending the preceding June 30."32 This is an unusual degree of inflation adjustment; no other federal land agency's payment program has this feature. But as will be shown below, increases in authorization do not necessarily lead to a commensurate increase in the funds received by the counties.

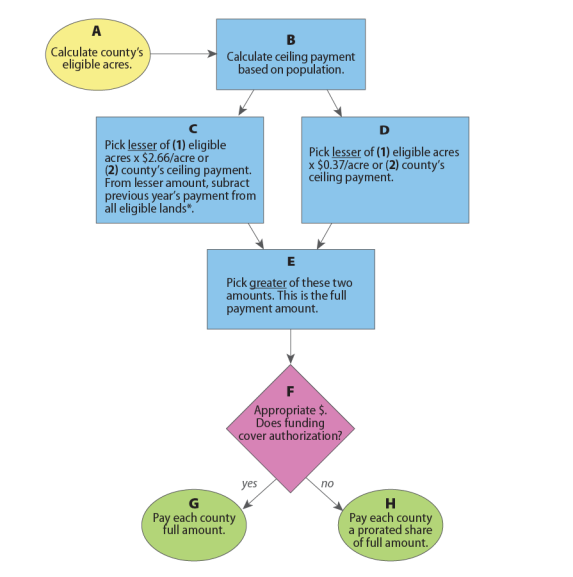

Putting It All Together: Calculating a County's Payment

With answers to these questions, the authorized payment level for a county can be calculated. (Figure 5 shows a flow chart of the steps in these comparisons.) Two options are possible; both must be determined for each county, and the payment is the higher of the two alternatives.

Alternative A. Which is less: the county's eligible acreage multiplied by $2.66 per acre or the county's ceiling payment based on its population? Pick the lesser of these two numbers. From it, subtract the previous year's total payments for these eligible lands under specific payment or revenue-sharing programs of the federal agencies that control the eligible land.33 The amount to be deducted is based on an annual report from the governor of each state to DOI. This option is called the standard rate.

Alternative B. Which is less: the county's eligible acreage multiplied by $0.37 per acre or the county's ceiling payment based on its population? Pick the lesser of these two. This option is called the minimum provision and is used in counties that received relatively large payments (more than $2.29 per acre for FY2017) from other federal agencies in the previous year.

The county is authorized to receive whichever of the above calculations—(A) or (B)—is greater. This calculation must be made for all counties individually to determine the national authorization level. If appropriations are insufficient for full funding, each county receives a pro rata share of the appropriation. For FY2017, the PILT appropriation of $465.0 million was 99.7% of the authorized level of $465.9. Thus, counties received 99.7% of the full formula amount.

The standard rate, with its offset between agency-specific payments and PILT payments, still does not guarantee a constant level of federal payments to counties because of the time lag in determining PILT payments. Federal payments for a given fiscal year generally are based on the receipts of the prior year. PILT payments of the following fiscal year are offset by these payments.

The combination of specific payments and PILT in the standard rate means that reductions (or increases) in those other payments in the previous year could be offset exactly by increases (or reductions) in PILT payments. However, provided the county's population is not so low as to affect the outcome, PILT payments could not fall below $0.37 per acre for FY2017 (see Alternative B, above), so the full offset occurs only when the other federal payments in the previous year total less than $2.29 per acre (i.e., the maximum payment of $2.64 per acre minus the $0.37 per acre minimum payment from PILT).34

To illustrate, consider a county whose only eligible federal lands are under FS jurisdiction. If the federal receipts on the FS lands dropped in FY2014 (compared with FY2013), authorized FS payments in FY2015 would fall. Authorized PILT payments will therefore increase to offset the drop—in FY2016. (This example assumes the PILT payment is calculated under the standard rate.) The counties will be authorized to receive at least $2.64 per acre from FS payments and PILT payments combined,35 but the two payments would not come in the same year. Consequently, if FS payments are falling from year to year, the combined payments in the given year would be less than $2.64 per acre, but if FS payments are rising, the authorized combined payment in the given year would be more than $2.64 per acre.

National Totals

Because of the need for annual data, a precise dollar figure cannot be given in advance for each year's PILT authorization level.36 Information from all 2,227 counties with eligible land in FY2016 was needed before an aggregate figure for the nation could be calculated for the most recent payment. The FY2016 appropriation contained in P.L. 114-113 was based on an estimate of the authorized amount, and ultimately provided 98.3% of full payment to each county.

Current Issues

Although the enactment of six years of mandatory spending put the issue of full funding to rest for a time, county governments show strong support for continuing the mandatory spending feature for PILT. This question of mandatory spending was the biggest issue facing the program from the 112th through the 114th Congresses. At the same time, with congressional debate over spending levels in general, support for greater or mandatory spending for PILT in the future may compete with proposals to modify or even eliminate PILT as a means of reducing federal deficits.

Congressional interest, after the 1994 revisions to PILT, has focused on the three areas cited above:

- whether to approve mandatory spending (either temporary or permanent) at the full amount or some fixed level;

- whether to reduce the program, either through lower discretionary appropriations or by changing the PILT formula; and

- whether to add or subtract lands from the list of those now eligible for PILT payments.

For a relatively small fraction of the federal or even departmental budget, PILT garners considerable attention, especially from local governments: (1) 2,227 counties had lands eligible for PILT payments in FY2016; (2) the average payment per county (many of which are sparsely populated) was $202,784; (3) although some counties with eligible lands received no payment (because they have very few federal lands and PILT makes no payments of less than $100), many received over $1 million and 25 counties received over $3 million.37 The resulting impact on budgets of local governments helps generate interest despite the small size of the PILT program compared to the federal budget as a whole. As PILT funding reverts to discretionary spending, counties with large federal land holdings may face more fiscal uncertainty.

Several more specific issues also are being debated in Congress or within county governments. Among them are the inclusion of Indian or other categories of lands; tax equivalency, especially for eligible urban lands; and payments affecting the NWRS.

Inclusion of Indian Lands

The inclusion of other lands (e.g., military lands generally or those of specific agencies such as the National Aeronautics and Space Administration) under the PILT program has been mentioned from time to time, and some counties with many acres of nontaxable Indian lands within their boundaries have long supported adding Indian lands to the list of lands eligible for PILT. Their primary arguments are that these lands receive benefits from the county, such as road networks, but Indian residents do not pay for these benefits with property taxes. However, the federal government does not actually own these lands.

The complexity of the PILT formula makes it very difficult to calculate the consequences of such a move, either for authorization levels or appropriation levels. Additionally, Congress would have to decide what sorts of Indian lands would be eligible for such payments and a variety of other complex issues.38 If some categories of Indian lands were to be added to those lands already eligible for PILT, Congress might wish to limit payments to counties with more than some minimum percentage of Indian lands within their borders. Regardless, even a very restrictive definition of Indian lands seems likely to add many millions of acres to those already eligible for PILT. Even if the criteria for eligibility were determined, it still would be difficult to anticipate the effect on authorization levels. To paint an extreme example, if all of the eligible Indian lands were in counties whose PILT payments already were capped due to the population ceiling, inclusion of Indian lands would have no effect on PILT authorization levels.

If mandatory spending of the full formula amount were in place, appropriations would go up to fund the newly eligible lands. If PILT payments are discretionary and annual appropriations are less than the authorized level, each county would receive a pro rata share of the authorized full payment level. Individual counties whose eligible acres had jumped markedly with the inclusion of Indian lands might receive substantially more than in the past. Other counties (particularly those with few or no eligible Indian acres) would receive a smaller fraction of the authorized amount as limited dollars would be distributed among more lands.

Inclusion of Urban Lands and Tax Equivalency

Some observers have wondered whether urban federal lands are included in the PILT program. The response is that urban lands are not excluded from PILT under the current law. For example, in FY2016, the counties in which Sacramento, Chicago, and Cleveland are found, as well as the District of Columbia, all received PILT payments (see Table 2), although the property tax on similar nonfederal lands likely would have been substantially greater.

|

County |

Eligible Acres |

FY2016 Appropriated Amount ($) |

||

|

Sacramento County (CA) |

|

|

||

|

Cook County (IL) |

|

|

||

|

Cuyahoga County (OH) |

|

|

||

|

Arlington County (VA) |

|

|

||

|

District of Columbia |

|

|

Source: National Summary, FY2016.

Notes: The urban counties and the District of Columbia were selected to show a wide range in the amount of eligible lands and resulting payments.

a. Under the PILT formula, Arlington County's 27 eligible acres (all under the National Park Service) would generate a payment of $71. However, under the law, no payment is made for amounts under $100.

Eastern counties, which tend to be small, rarely have both large populations and large eligible acreage in the same county. By contrast, western counties tend to be very large and may have many eligible acres, and some, like Sacramento, may have large populations as well. Furthermore, as the cases of Arlington County and the District of Columbia illustrate, PILT payments are by no means acting as an equivalent to property tax payments. If the 8,482 acres in the District of Columbia or the 27 acres in Arlington County were owned by taxable entities, those acres would result in much more than $22,007 or $0, respectively, in property taxes.39

Because the formula in PILT does not reflect property taxes, counties such as these might support a revised formula that would approach property tax payments.

National Wildlife Refuge System Lands

As noted above, NWRS lands that were withdrawn from the public domain are eligible for PILT, and those that were acquired are not. In addition, the National Wildlife Refuge Fund (NWRF, also called the Refuge Revenue-Sharing Fund, or RRSF) relies on annual appropriations for full funding. For FY2016, payments for NWRF were approximately 23% of the authorized level. For refuge lands eligible for PILT, some or perhaps all of the NWRF payment will be made up for in the following year's PILT payment, but this will not occur for acquired lands because they are not eligible for PILT. Congress may consider making all refuge lands eligible for PILT and/or providing mandatory spending for NWRF, as it has for PILT. Eastern counties could be the largest beneficiaries of such a change, although some western states also may have many NWRS acres that currently are not eligible for PILT. (See Table 3 for selected state examples.) Adding the 9.8 million acres of NWRS lands under the primary jurisdiction of FWS but currently ineligible for PILT would increase PILT lands by about 1.6%.

|

State |

NWRS Acres Reserved from |

Total NWRS Acres |

Percent Eligible |

||||

|

Alabama |

|

|

|

||||

|

Arizona |

|

|

|

||||

|

Iowa |

|

|

|

||||

|

Maine |

|

|

|

||||

|

Montana |

|

|

|

||||

|

Ohio |

|

|

|

||||

|

Oregon |

|

|

|

Source: Compiled from Annual Report of Lands Under Control of the U.S. Fish and Wildlife Service As of September 30, 2015 (the most recent year available).

Notes: States were selected to show a wide range in NWRS acreage and amount of public domain lands. NWRS = National Wildlife Refuge System; PILT = Payments in Lieu of Taxes.

County Uncertainty and Fiscal Effects on Counties40

The PILT program, when it was a mandatory spending program, provided a relatively certain flow of funds to recipient jurisdictions. Some observers and policymakers are concerned that using discretionary spending for PILT or the elimination of the program could destabilize the fiscal structure of some jurisdictions receiving PILT payments.41 Nationally, the relative size of the PILT payments would seem to mitigate the impact and PILT reductions would not seem to have a measurable fiscal impact on most county budgets that receive PILT transfers. Locally, however, the impacts may be greater—in some jurisdictions, perhaps substantially.

Reliance on property taxes is important for most counties. Nationwide, in FY2013, local property taxes (for counties, cities, and special districts) comprised roughly 46.8% of own-source revenue or just over $452 billion in total revenues.42 However, in the same year, the PILT program was very much smaller: the appropriated $400.2 million in PILT payments was less than 0.1% of property tax revenue nationally.43 For the 25 counties that received over $3 million in FY2016, the government services provided by the county could be adversely affected in the near term (although restructuring the property tax or raising other local fees or taxes could likely compensate for the reduced federal payment). Smaller payments also would be important in low-property-value, low-population counties with relatively greater shares of federally owned land.

Appendix. PILT Data Tables

The first two tables below show the data presented in Figure 1 and Figure 2. The third shows the agency payments that offset payments under PILT in the following year.

Table A-1. Total PILT Payments, FY1993-FY2017: Appropriations in Current and Inflation-Adjusted 2017 Dollars

($ in millions)

|

Year |

Appropriation |

Inflation-Adjusted Appropriation |

||

|

1993 |

|

161.7 |

||

|

1994 |

|

159.6 |

||

|

1995 |

|

151.8 |

||

|

1996 |

|

166.2 |

||

|

1997 |

|

163.8 |

||

|

1998 |

|

170.0 |

||

|

1999 |

|

175.8 |

||

|

2000 |

|

185.1 |

||

|

2001 |

|

269.1 |

||

|

2002 |

|

278.1 |

||

|

2003 |

|

285.0 |

||

|

2004 |

|

285.6 |

||

|

2005 |

|

279.6 |

||

|

2006 |

|

278.0 |

||

|

2007 |

|

270.5 |

||

|

2008 |

|

418.3 |

||

|

2009 |

|

430.2 |

||

|

2010 |

|

399.3 |

||

|

2011 |

|

410.7 |

||

|

2012 |

|

422.2 |

||

|

2013 |

|

422.8 |

||

|

2014 |

|

453.7 |

||

|

2015 |

|

450.7 |

||

|

2016 |

|

457.9 |

||

|

2017 |

|

465.0 |

Sources: Current dollars from each annual National Summary.

Notes: Inflation adjustment is based on chain-type price index. FY2016 is presented in current dollars.

For the same data in a bar chart, see Figure 1.

|

Year |

Authorized |

Appropriated |

|

1993 |

103.2 |

103.2 |

|

1994 |

104.4 |

104.1 |

|

1995 |

130.5 |

101.1 |

|

1996 |

165.1 |

112.8 |

|

1997 |

212.0 |

113.1 |

|

1998 |

260.5 |

118.8 |

|

1999 |

303.7 |

124.6 |

|

2000 |

317.6 |

134.0 |

|

2001 |

338.6 |

199.2 |

|

2002 |

350.8 |

209.4 |

|

2003 |

324.1 |

218.6 |

|

2004 |

331.3 |

224.7 |

|

2005 |

332.0 |

226.8 |

|

2006 |

344.4 |

232.5 |

|

2007 |

358.3 |

232.5 |

|

2008 |

367.2 |

367.2 |

|

2009 |

381.6 |

381.6 |

|

2010 |

358.1 |

358.1 |

|

2011 |

375.2 |

375.2 |

|

2012 |

393.0 |

393.0 |

|

2013 |

421.7 |

400.2 |

|

2014 |

436.9 |

436.9 |

|

2015 |

451.5 |

439.5 |

|

2016 |

459.5 |

452.0 |

|

2017 |

465.9 |

465.0 |

Sources: Relevant annual National Summary reports.

Notes: For the same data in a bar chart, see Figure 2.

|

Federal Agency Making Payment |

Short Title of Law or Common Name |

P.L. or Date |

U.S. Stat. |

U.S. Code |

Lands Eligible for Payments |

Payment Rate |

|

Forest Service |

25% payments or Payments to States |

Act of May 23, 1908 (ch. 192, §13) |

35 Stat. 260 |

16 U.S.C. §500 |

All national forest (NF) lands |

25% of gross receipts to state for roads and schools in counties |

|

None |

Act of June 20, 1910 (ch. 310) |

36 Stat. 557, §6 |

Not codified |

NF lands in AZ and NM |

Proportion of lands in NFs reserved for schools times proceeds from sales in NF |

|

|

None |

Act of June 22, 1948 (ch. 593, §5); Act of June 22, 1956 (ch. 425, §2) |

62 Stat. 570, |

16 U.S.C. §577g, §577g-1 |

Lands in Superior NF, MN |

0.75% of appraised value (in addition to 25% payments above) |

|

|

Mineral Leasing Act for Acquired Lands (§6) |

Act of Aug. 7, 1947 |

61 Stat. 915 |

30 U.S.C. §355 |

NF lands with mineral leasing |

50% of mineral leasing revenues to states for counties |

|

|

Material Disposal Act |

Act of July 31, 1947 (§3) |

61 Stat. 681 |

30 U.S.C. §603 |

Net revenues from sale of land and materials |

Varies depending on type of receipt and agency |

|

|

Secure Rural Schools and Community Self-Determination Acta |

P.L. 106-393, as amended |

114 Stat. 1607, as amended |

16 U.S.C. §§7101 et seq. |

NF lands (but not lands under Land Utilization Program [LUP] or National Grasslands) if this option is chosen by county instead of 25% payments |

Complex formula; see CRS Report R41303, Reauthorizing the Secure Rural Schools and Community Self-Determination Act of 2000, by [author name scrubbed] |

|

|

Bankhead-Jones Farm Tenant Act |

Act of July 22, 1937 (ch. 513, §33) |

50 Stat. 526 |

7 U.S.C. §1012 |

National Grasslands and LUP lands managed by FSb |

25% of revenues for use of lands to states |

|

|

Bureau of Land Management |

Mineral Lands Leasing Act |

Act of February 25, 1920 (ch. 85, §35) |

41 Stat. 450 |

30 U.S.C. §191 |

Public lands |

50% of leasing revenues to states for counties |

|

Taylor Grazing Act |

Act of June 28, 1934 (ch. 865, §10) |

48 Stat. 1273 |

43 U.S.C. §315i |

Public lands |

12.5% of grazing receipts to states for counties |

|

|

Bankhead-Jones Farm Tenant Act |

Act of July 22, 1937 (ch. 513, §33) |

50 Stat. 526 |

7 U.S.C. §1012 |

National Grasslands and LUP lands managed by BLM |

25% of revenues for use of lands to states |

|

|

Mineral Leasing Act for Acquired Lands (§6) |

Act of Aug. 7, 1949 |

61 Stat. 915 |

30 U.S.C. §355 |

Public lands with mineral leasing |

50% of mineral leasing revenues to states for counties |

|

|

Material Disposal Act |

Act of July 31, 1947 (§3) |

61 Stat. 681 |

30 U.S.C. §603 |

Net revenues from sale of land and materials |

Varies depending on type of receipt and agency |

|

|

Fish and Wildlife Service |

Refuge Revenue Sharing Act |

Act of June 15, 1935 (ch. 261, §401(c)(2)) |

49 Stat. 383 |

16 U.S.C. §715s(c)(2) |

Public domain lands in NWRSc |

25% of net receipts from timber, grazing, and mineral sales directly to county; remaining 75% to counties under other formulas |

|

Federal Energy Regulatory Commission |

Federal Power Act |

Act of June 10, 1920, (ch. 285, §17) |

41 Stat. 1072 |

16 U.S.C. §810 |

NF and public lands with occupancy and use for power projects |

37.5% of revenues from licenses for occupancy and use to states for counties |

Sources: 31 U.S.C. §6903(a)(1), National Summary, FY2017, p. 13. The latter document has typographical errors that are corrected here, as noted. Because the various payment laws are identified in some documents by title, in others by a U.S. Code citation, and in still others by the Statutes at Large, date, or Public Law, all of these are cited here, where they exist.

a. When payments are made for lands under FS jurisdiction for the Secure Rural Schools (SRS) program, the payments result in a reduction (offset) in the following year's PILT payment. However, if the lands are under BLM jurisdiction, no offset is made in the following year's PILT payment. All BLM lands eligible for SRS payments are in Oregon.

b. The table shown in National Summary, FY2017, p. 13, indicates that these payments are made only to BLM lands and omits mention of FS lands. However, the majority of Bankhead-Jones lands are in the FS National Grasslands, and DOI makes payments for these lands regardless of which of the two agencies own them. Therefore, this payment is shown in the table for both agencies.

c. Acquired lands in the National Wildlife Refuge System (NWRS) are not eligible for PILT payments. See "National Wildlife Refuge System Lands" above.