Introduction

The Earned Income Tax Credit (EITC) is a refundable tax credit available to eligible workers with relatively low earnings. Because the credit is refundable, an EITC recipient need not owe taxes to receive the benefit. The credit is authorized by Section 32 of the Internal Revenue Code (IRC) and administered as part of the federal income tax system. For tax year 2014 (returns filed in 2015), a total of $68.3 billion was claimed by 28.5 million tax filers, making the EITC the largest need-tested antipoverty cash assistance program.

Under current law, the EITC is calculated based on a recipient's earned income, using one of eight different formulas, which vary depending on several factors, including the number of qualifying children a tax filer has (zero, one, two, or three or more) and his or her marital status (unmarried or married). All else being equal, the amount of the credit tends to increase with the number of eligible children the EITC claimant has. Indeed, most of the benefits of the EITC—97% of EITC dollars for 2014—go to families with children.

Two temporary modifications to the EITC were enacted under the American Recovery and Reinvestment Act of 2009 (ARRA; P.L. 111-5), extended by P.L. 111-312 and P.L. 112-240, and made permanent by the Protecting Americans from Tax Hikes (PATH) Act (Division Q of P.L. 114-113). The first modification was a larger credit for families with three or more children, while the second reduced the EITC's marriage penalty.

This report provides an overview of the EITC, first discussing eligibility requirements for the credit, followed by how the credit is computed and paid. The report then provides data on the growth of the EITC since it was first enacted in 1975. Finally the report concludes with data on the EITC claimed on 2014 tax returns, examining EITC claims by number of qualifying children, income level, tax filing status, and location of residence.

Eligibility for the EITC

A tax filer must fulfill the following requirements to claim the EITC:

- 1. The tax filer must file a federal income tax return.1

- 2. The tax filer must have earned income.

- 3. The tax filer must meet certain residency and identification requirements.

- 4. The tax filer's children must meet relationship, residency, and age requirements to be considered qualifying children for the credit.

- 5. Childless workers who claim the credit must be between ages 25 and 64. (This age requirement does not apply to EITC claimants with qualifying children.)

- 6. The tax filer's investment income must be below a certain amount.

- 7. The tax filer must not be disallowed the credit due to prior fraud or reckless disregard of the rules when they previously claimed the EITC.

Additionally, a tax filer with income above a certain dollar amount (labelled as "income where credit = 0" in Table 1) will be ineligible for the credit. Given that this income level is dependent on the number of qualifying children and marital status of the tax filer, this requirement is discussed in greater detail in the section of the report entitled "Calculating the EITC."

Requirements (1) through (7) are discussed in detail below.

Filing a Federal Income Tax Return

To be eligible for the EITC, a person must file a federal income tax return. Those who do not file a federal income tax return cannot receive the EITC.

The EITC can be claimed by taxpayers filing their tax return as married filing jointly, head of household, or single.2 Tax filers cannot claim the EITC if they use the filing status of married filing separately. If the tax filer has a qualifying child, the tax filer must include the child's name and Social Security number on a separate schedule (Schedule EIC) filed with the federal tax return.3

Earned Income

A tax filer must have earned income to claim the EITC. Earned income for the EITC is defined as wages, tips, and other compensation included in gross income. It also includes net self-employment income (self-employment income after deduction of one-half of Social Security payroll taxes paid by a self-employed individual).

In addition, servicemembers may elect to include combat pay in their earnings when calculating the EITC. All income earned by a member of the Armed Forces while in a designated combat zone is considered combat pay and is normally not included in taxable income. However, a tax filer may elect to include combat pay as earnings for the purpose of calculating the EITC.4 Generally, servicemembers will make this election if it results in a larger credit. (Using combat pay to calculate the EITC does not make the combat pay taxable income.)

Certain forms of income are not considered earnings for the purpose of the EITC. These include pension and annuity income, income of nonresident aliens not from a U.S. business, income earned while incarcerated for work in a prison, and TANF benefits paid in exchange for participation in work experience or community service activities.

Finally, tax filers who claim the foreign earned income exclusion (i.e., they file Form 2555 or Form 2555EZ with their federal income tax return) are ineligible to claim the EITC.5

Residency and Identification Requirements

Under current law, an EITC recipient must be a resident of the United States, unless the recipient resides in another country because of U.S. military service. To be eligible for the credit, the tax filer must provide valid Social Security numbers (SSNs) for work purposes6 for themselves, spouses if married filing jointly, and any qualifying children. (U.S. citizenship is not required to be eligible for the credit. SSNs do not indicate U.S. citizenship.) Nonresident aliens—those who do not have green cards or do not spend sufficient time in the United States—are generally ineligible for the EITC.7

Qualifying Children

An EITC recipient's qualifying child must meet three requirements.8 First, the child must have a specific relationship to the tax filer (son, daughter, step child or foster child,9 brother, sister, half-brother, half-sister, step brother, step sister, or descendent of such a relative). Second, the child must share a residence with the taxpayer for more than half the year in the United States.10 Third, the child must meet certain age requirements; namely, the child must be under the age of 19 (or age 24, if a full-time student) or be permanently and totally disabled.

As a result of these three requirements, a child may be the qualifying child of more than one tax filer in the same household. For example, a child who lives with a single parent, grandparent, and aunt in the same home could be a qualifying child of all three of these individuals. But only one of these individuals can claim the qualifying child for the EITC, and the others cannot. Indeed, it appears that under current law, the other individuals are also ineligible to claim the childless EITC.11 In the case where the tax filers cannot agree on who claims the child, there are "tie-breaker" rules for who can claim the child for the EITC.12

Age Requirements for EITC Recipients with No Qualifying Children

If a tax filer has no qualifying children, he or she must be between 25 and 64 years of age to be eligible for the EITC. There is no age requirement for tax filers with qualifying children.

Investment Income

A tax filer with investment income over a certain dollar amount is ineligible for the EITC. The statutory limit—$2,200—is adjusted annually for inflation. For 2017, the limit on investment income is $3,450. Investment income is defined as interest income (including tax-exempt interest), dividends, net rent, net capital gains, and net passive income. It also includes royalties that are from sources other than the filer's ordinary business activities.

Disallowance of the EITC Due to Fraud or Reckless Disregard of Rules

A tax filer is barred from claiming the EITC for a period of 10 years after the IRS makes a final determination to reduce or disallow a tax filer's EITC because that individual made a fraudulent EITC claim. A tax filer is barred from claiming the EITC for a period of two years after the IRS determines that the individual made an EITC claim "due to reckless and intentional disregard of the rules" of the EITC, but that disregard was not found to be fraud.13

Calculating the EITC

The EITC amount is based on formulas that consider earned income, number of qualifying children, marital status, and adjusted gross income (AGI). In general, the EITC equals a fixed percentage (the "credit rate") of earned income until the credit reaches its maximum amount. The EITC then remains at its maximum level over a subsequent range of earned income, between the "earned income amount" and the "phase-out amount threshold." Finally, the credit gradually decreases in value to zero at a fixed rate (the "phase-out rate") for each additional dollar of earnings or AGI (whichever is greater) above the phase-out amount threshold. The specific values of these EITC parameters (e.g., credit rate, earned income amount, etc.) vary depending on several factors, including the number of qualifying children a tax filer has and his or her marital status, as illustrated in Table 1.

|

Number of Qualifying Children |

0 |

1 |

2 |

3 or more |

|

unmarried tax filers (single and head of household filers) |

||||

|

credit rate |

7.65% |

34% |

40% |

45% |

|

earned income amount |

$6,670 |

$10,000 |

$14,040 |

$14,040 |

|

maximum credit amount |

$510 |

$3,400 |

$5,616 |

$6,318 |

|

phase-out amount threshold |

$8,340 |

$18,340 |

$18,340 |

$18,340 |

|

phase-out rate |

7.65% |

15.98% |

21.06% |

21.06% |

|

income where credit = 0 |

$15,010 |

$39,617 |

$45,007 |

$48,340 |

|

married tax filers (married filing jointly) |

||||

|

credit rate |

7.65% |

34% |

40% |

45% |

|

earned income amount |

$6,670 |

$10,000 |

$14,040 |

$14,040 |

|

maximum credit amount |

$510 |

$3,400 |

$5,616 |

$6,318 |

|

phase-out amount threshold |

$13,930 |

$23,930 |

$23,930 |

$23,930 |

|

phase-out rate |

7.65% |

15.98% |

21.06% |

21.06% |

|

income where credit = 0 |

$20,600 |

$45,207 |

$50,597 |

$53,930 |

Source: IRS Revenue Procedure 2016-55 and Internal Revenue Code (IRC) Section 32.

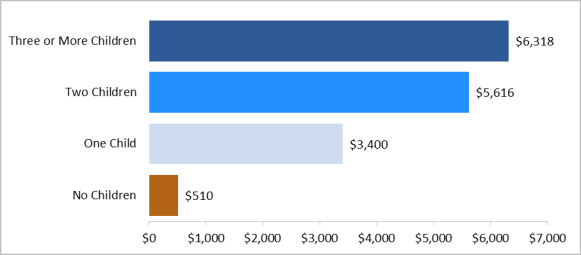

As illustrated in Table 1, the EITC's earned income amounts, credit rates, phase-out rates, and maximum credit amounts vary by the number of qualifying children a tax filer has. The EITC ranges from a maximum credit of $510 for a tax filer without a child to $6,318 for a tax filer with three or more qualifying children, as illustrated in Figure 1.

|

Figure 1. Maximum EITC by Number of Qualifying Children: 2017 |

|

|

Source: Congressional Research Service based on IRS Revenue Procedure 2016-55 and Internal Revenue Code (IRC) Section 32. |

The phase-out amount threshold varies by both the number of qualifying children a tax filer has and his or her marital status. The phase-out amount threshold for those who are married filing joint returns is $5,590 greater than for unmarried filing statuses with the same number of children. (Tax filers who file as married filing separately are ineligible for the EITC.) This higher phase-out amount threshold for married tax filers reduces (but generally does not eliminate) potential "marriage penalties" in the EITC whereby the credit for a married couple is less than the combined credit of two unmarried recipients.

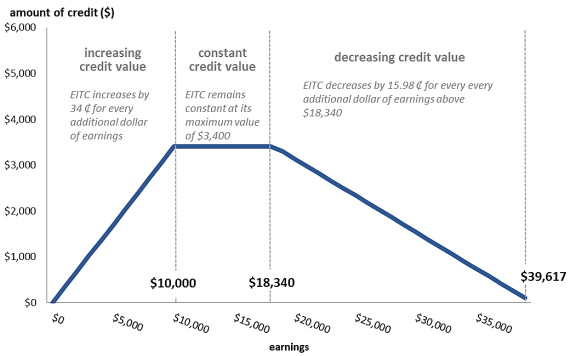

Figure 2 illustrates the EITC amount by earnings level for an unmarried taxpayer with one child for 2017. It shows the three distinct ranges of EITC for this family:

- Phase-in Range: The EITC increases with earnings from the first dollar of earnings up to earnings of $10,000. Over this earnings range, the credit equals the credit rate (34% for a tax filer with one child) times the amount of annual earnings. The $10,000 threshold is called the earned income amount and is the earnings level at which the EITC ceases to increase with earned income. The income interval up to the earned income amount, where the EITC increases with earnings, is known as the phase-in range.

- Plateau: The EITC remains at its maximum level of $3,400 from the earned income amount ($10,000 until earnings exceed $18,340). The $3,400 credit represents the maximum credit for a tax filer with one child in 2017. The income interval with the EITC fixed at its maximum value represents the plateau on Figure 2.

- Phase-out Range: Once earnings exceed $18,340, the EITC is reduced for every additional dollar over that amount. The $18,340 threshold is known as the phase-out amount threshold for a single taxpayer with one child in 2017. For each dollar over the phase-out amount threshold, the EITC is reduced by 15.98%. The 15.98% rate is known as the phase-out rate. The income interval from the phase-out income level until the EITC is completely phased out is known as the phase-out range.

The EITC is completely phased out (EITC = $0) once the tax filer's AGI (or earned income, whichever is greater) reaches $39,617. The earned income amounts and the phase-out amount thresholds are adjusted each year for inflation.

In practice, EITC claimants use tables published by the IRS to calculate their credit amount. A tax filer can look up the correct amount of his or her EITC based on income, marital status, and number of qualifying children. The instructions for the federal income tax form14 show the EITC amounts in tables by income brackets (in $50 increments).

Income Limits for the EITC

As previously discussed, the amount of the EITC is reduced for each dollar of AGI (or earnings, if greater) above a certain dollar threshold, referred to as the phase-out amount threshold. That threshold, combined with the phase-out rate, results in a specific income level (referred to as "income where credit = 0" in Table 1) above which a tax filer is ineligible for the credit. This income level, where the credit reaches zero, is sometimes referred to as the eligibility threshold.

As illustrated in Table 1, there are eight eligibility thresholds for the EITC depending on the number of qualifying children a taxpayer has and his or her marital status. The eligibility thresholds vary every year given that they are based in part on a parameter of the credit—the phase-out amount threshold—that is explicitly adjusted for inflation. Table 2 shows the EITC eligibility thresholds for 2017. An EITC claimant's AGI (or earnings, if higher) must be below these thresholds for the claimant to qualify for the EITC. In 2017, these thresholds range from $15,010 for an unmarried tax filer with no qualifying child to $53,930 for a married tax filer filing jointly with three or more qualified children.

Table 2 expresses these eligibility thresholds as a percentage of the 2017 poverty guidelines. For example, the poverty guideline for a family of three in 2016 was $20,420. Families of three with income at or below this amount are considered poor. The EITC eligibility threshold of $45,007 for an unmarried person filing jointly with two qualifying children was more than twice (220.4%) the poverty guideline for a family of that type.

Table 2 also expresses these eligibility thresholds as a percentage of the earnings of one worker who works a minimum wage job ($7.25 per hour) 40 hours per week, 52 weeks a year ($15,080 annually). For the purposes of the calculations in Table 2, married EITC recipients are assumed to have the same aggregate annual earnings as unmarried recipients—$15,080. The EITC is available in 2017 to all families at this earnings level except an unmarried taxpayer with no children. The EITC was available to families with children who had earnings between 2.6 to 3.6 times the annual earnings from a minimum wage job (262.7% to 357.6% of $15,080).

Table 2. Maximum AGI to Qualify for the EITC, by Number of Qualifying Children and Filing Status in 2017

|

No Qualifying Children |

One Qualifying Child |

Two Qualifying Children |

Three or More Qualifying Children |

||

|

Unmarried |

$15,010 |

$39,617 |

$45,007 |

$48,340 |

|

|

Married Filing Jointly |

20,600 |

45,207 |

50,597 |

53,930 |

|

|

As a percentage of the poverty threshold |

|

||||

|

Unmarried |

124.5% |

243.9% |

220.4% |

196.5%a |

|

|

Married Filing Jointly |

126.8 |

221.4 |

205.7 |

187.4b |

|

|

As a percentage of work at the federal minimum wage, 40 hours per week, 52 weeks per year |

|||||

|

Unmarried |

99.5% |

262.7% |

298.5% |

320.6% |

|

|

Married Filing Jointly |

136.6 |

299.8 |

335.5 |

357.6 |

|

Source: Congressional Research Service calculations based on IRS Revenue Procedure 2016-55, Internal Revenue Code (IRC) Section 32 and the 2017 Poverty Guidelines available at https://aspe.hhs.gov/poverty-guidelines.

a. Represents the EITC AGI threshold divided by the poverty guidelines for a family of 4

b. Represents the EITC AGI threshold divided by the poverty guidelines for a family of 5.

Payment of the EITC

The EITC is provided to individuals and families annually in a lump sum payment after a taxpayer files a federal income tax return.15 It may be received in one of three ways:

- 1. a reduction in federal tax liability;

- 2. a cash payment from the Treasury if the tax filer has no tax liability, through a tax refund check; or

- 3. a combination of reduced federal tax liability and a refund.

The majority (86%) of the aggregate amount of the EITC—$68.3 billion for 2014—is received as a refund.16 In other words, $58.9 billion of the EITC was received as a refund for 2014, while approximately $9.5 billion offset tax liabilities.

The EITC is taken against all taxes reported17 on the federal individual income tax return (Form 1040) after all nonrefundable credits have been taken. On the tax form, the EITC can be found in the payments section after the lines for withholding and estimated tax payments.

The EITC benefits families when they file their income taxes. Thus, payments are generally based on the prior year's income, earnings, and family composition. That is, the EITC earned in 2017, based on a tax filer's earnings, income, and family composition, will be paid in 2018.18 If the tax filer is owed a refund, and that filer's return includes an EITC, that refund will be made on or after February 15.19

Interaction with Other Tax Provisions

On the tax return, the EITC is calculated after total tax liability and all nonrefundable credits. Nonrefundable tax credits, which are taken against (reduce) income tax liability, include credits for education, dependent care, savings, and the nonrefundable portion of the child credit.20 If an EITC-eligible family has a tax liability and can use one or more of these credits, the total amount of their EITC will remain unchanged, but how they receive the credit will change. If nonrefundable tax credits can reduce a family's tax liability, a greater amount of their EITC will be received as a refund, and less will offset their tax liability since their tax liability is smaller.

For tax filers whose income places them in the "phase-out range" of the credit, reducing their income (all else being unchanged) will result in a larger EITC. (As illustrated in Figure 2, reducing income when a tax filer is in the phase-out range results in the tax filer increasing the amount of the credit they receive.) A variety of forms of income can be excluded from both AGI and earned income, reducing a taxpayer's AGI or earned income for purposes of calculating the credit. For example, pretax contributions to savings accounts for retirement or medical expenses are not included in either AGI or earned income. Hence, by making these contributions, EITC claimants whose precontribution income places them in the phase-out range of the credit will reduce their AGI or earned income for purposes of calculating the EITC and thus receive a larger credit.21

In contrast, for tax filers whose income places them in the "phase-in range" of the credit, reducing their income (all else unchanged) will result in a smaller EITC. (As illustrated in Figure 2, reducing income when a tax filer is in the phase-in range results in the tax filer reducing the amount of the credit they receive.) Generally, nontaxable income cannot be included in earned income for purposes of calculating the EITC. However, as previously discussed, servicemembers may elect to include their nontaxable combat pay as earnings, for purposes of calculating the EITC. Generally, servicemembers whose income (excluding their combat pay) places them in the phase-in range will elect to include their combat pay in earned income for purposes of calculating the EITC in order to receive a larger credit.

Treatment of the EITC for Need-Tested Benefit Programs

By law,22 the EITC cannot be counted as income in determining eligibility for, or the amount of, any federally funded public benefit program including Supplemental Nutrition Assistance Program (SNAP) food assistance, low-income housing, Medicaid, Supplemental Security Income (SSI), and Temporary Assistance for Needy Families (TANF). An EITC refund that is saved by the filer does not count against the resource limits of any federally funded public benefit program for 12 months after the refund is received.

Modifications to the EITC Made Permanent by

P.L. 114-113

Two temporary modifications to the EITC were enacted by the American Recovery and Reinvestment Act of 2009 (ARRA; P.L. 111-5). First, ARRA enacted a temporary larger credit for families with three or more children by creating a new higher credit rate of 45% (previously, these tax filers were eligible for a credit rate of 40%). Second, ARRA expanded marriage penalty relief by increasing the earnings level at which the credit phased out for married tax filers in comparison to unmarried tax filers with the same number of children. Before ARRA, the EITC for married tax filers would begin to phase out for earnings $3,000 (adjusted for inflation) greater than the level for unmarried recipients with the same number of children. ARRA increased this differential to $5,000 (adjusted for inflation). In 2017, this marriage penalty relief was equal to $5,590. These two changes were originally scheduled to be in effect only for 2009 and 2010. The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312) extended these ARRA provisions for two years (2011 and 2012). The American Taxpayer Relief Act (ATRA; P.L. 112-240) extended the ARRA provisions for five more years (2013-2017). The Protecting Americans from Tax Hikes (PATH) Act (Division Q of P.L. 114-113) made these two modifications permanent.

Participation and Benefits

The EITC was first enacted in 1975 as a temporary measure meant to encourage economic growth in the face of the 1974 recession and rising food and energy prices. It was also originally intended to "assist in encouraging people to obtain employment, reducing the unemployment rate, and reducing the welfare rolls."23 Over time the list of EITC objectives has grown to include poverty reduction. Today the EITC is the largest need-tested, cash benefit antipoverty program. This section first provides a historical overview of the growth of the EITC for tax years 1975 to 2014; it then examines information on EITC participation for 2014.

Trends in Participation and EITC Benefits

When originally enacted by the Tax Reduction Act of 1975 (P.L. 94-12), the EITC was a temporary refundable tax credit in effect for 1975. For that year, 6.2 million tax filers claimed the EITC and the total EITC amount claimed was $1.25 billion (in constant 2014 dollars, this equals $5.5 billion). The credit was extended several more times on a temporary basis and made permanent by the Revenue Act of 1978 (P.L. 95-600). Legislation enacted in 1986 (P.L. 99-514), 1990 (P.L. 101-508), 1993 (P.L. 103-66), 2001 (P.L. 107-16), and 2009 (P.L. 111-5) increased the amount of the credit by changing the credit formula.

Before 1990, the credit amount was calculated as a percentage of earnings ("the credit rate") up until the earned income amount. The credit then remained at its maximum level before gradually decreasing in value as earnings increased. Legislative changes to the credit made during this time generally increased the amount of the credit in a variety of ways including increasing the credit rate, increasing the earned income amount, increasing the phase-out amount threshold, and decreasing the phase-out rate. Nonetheless, the credit amount depended on earned income.

Beginning in 1990 and more substantially in 1993, the credit formula was revised such that the credit amount varied based on earnings and, to a certain extent, the number of qualifying children. This essentially increased the credit by family size. In addition, for the first time in 1993, Congress made workers without qualifying children eligible for the EITC, although the credit was smaller than the credit for claimants with qualifying children.

In 2001, the credit formula was revised again so that it also varied based in part on marital status. As a result of this change, often referred to as "marriage penalty relief," certain married tax filers would receive a larger credit than unmarried tax filers with the same number of children. In 2009, the marriage penalty relief was expanded further and a larger credit was created for families with three or more children. These 2009 changes were extended several times and made permanent by P.L. 114-113.

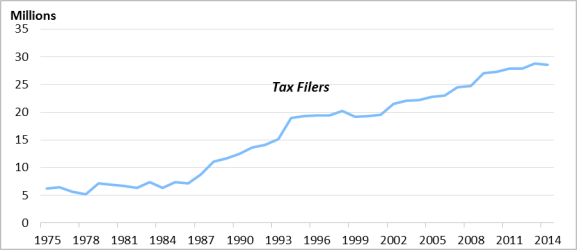

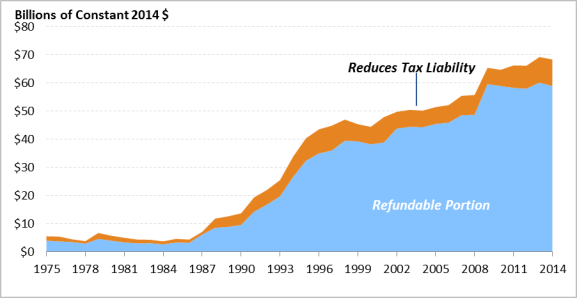

Figure 3 shows the number of tax filers claiming the EITC for 1975 to 2014. Figure 4 shows the amount of the EITC claimed on these returns, with dollar amounts adjusted for inflation to represent 2014 dollars. The figures show the effects of the legislative expansions of the EITC, with the credit experiencing growth in the late 1980s through the mid-1990s and then again in the 2000s. As shown on Figure 4, throughout the history of the EITC, most credits have been paid in the form of refunds, with a relatively small share of the EITC reducing regular federal income tax liability.

|

Figure 3. Number of Tax Filers Claiming the EITC: 1975 to 2014 |

|

|

Source: Congressional Research Service. For pre-2003 data, U.S. Congress, House Committee on Ways and Means, 2004 Green Book, Background Material and Data on Programs Within the Jurisdiction of the Committee on Ways and Means, 108th Congress, 2nd session, WMCP 108-6, March 2004, pp. 13-41. For 2003 and later data, Internal Revenue Service, Total File, United States, Individual Income and Tax Data, by State and Size of Adjusted Gross Income, 2003 through 2014, expanded unpublished version, Table 2.5. Note: For a tabular display of this information, see Table A-1. |

|

Figure 4. EITC Claimed on Federal Income Tax Returns: 1975-2014 |

|

|

Source: Congressional Research Service. For pre-2003 data, U.S. Congress, House Committee on Ways and Means, 2004 Green Book, Background Material and Data on Programs Within the Jurisdiction of the Committee on Ways and Means, 108th Congress, 2nd session, WMCP 108-6, March 2004, pp. 13-41. For 2003 and later data, Internal Revenue Service, Total File, United States, Individual Income and Tax Data, by State and Size of Adjusted Gross Income, 2003 through 2014, expanded unpublished version, Table 2.5. Notes: Constant 2014 dollars were computed using the Consumer Price Index for all Urban Consumers (CPI-U). For a tabular display of this information, see Table A-1. |

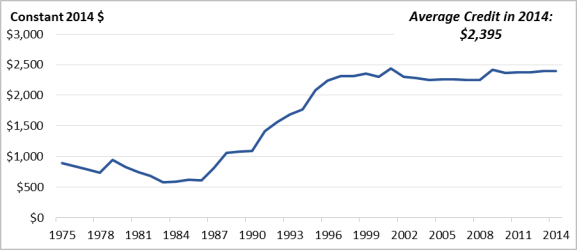

The growth in the total amount of EITC claimed in the late 1980s to the mid-1990s was due to increases not only in participation, but also in the average credit received by tax filers. Figure 5 shows the average EITC claimed for 1975 to 2014, in inflation-adjusted (2014) dollars. Before the 1986 Tax Reform Act (P.L. 99-514), EITC thresholds were not indexed for inflation, and the average credit lost value each year. However, the 1986 act increased the monetary parameters of the credit for prior inflation and adjusted the threshold amounts and maximum credits annually for inflation in future years. The credit formula was also revised in 1990 and then again in 1993 such that the amount of the credit depended to a certain extent on family size. These changes resulted in an increasing average credit between the late 1980s and late 1990s. Since then, the average credit has largely maintained its real value. However, increases in the average credit amount in 2001 and 2009 were likely due to legislative changes that included larger credits for some married claimants and for families with three or more children.24 The average EITC claimed for 2014 was $2,395.

|

|

Source: Congressional Research Service. For pre-2003 data, U.S. Congress, House Committee on Ways and Means, 2004 Green Book, Background Material and Data on Programs Within the Jurisdiction of the Committee on Ways and Means, 108th Congress, 2nd session, WMCP 108-6, March 2004, pp. 13-41. For 2003 and later data, Internal Revenue Service, Total File, United States, Individual Income and Tax Data, by State and Size of Adjusted Gross Income, 2003 through 2014, expanded unpublished version, Table 2.5. Notes: Constant 2014 dollars were computed using the Consumer Price Index for all Urban Consumers (CPI-U). For a tabular display of this information, see Table A-1. |

Participation and EITC Amounts Claimed for 2014

For 2014, $68.3 billion of the EITC was claimed on 28.5 million tax returns.

Number of Qualifying Children

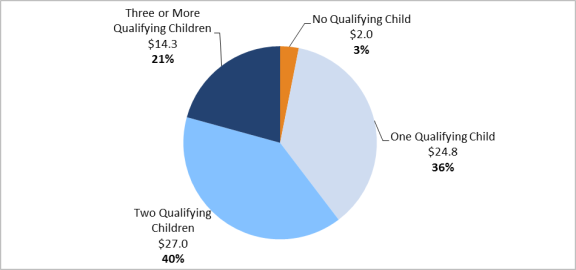

Most tax filers claiming the EITC, and those who received the most EITC dollars, were families with children. Figure 6 shows total EITC dollars claimed for 2014 by number of qualifying children. For 2014, 3% of all EITC dollars were claimed by tax filers with no qualifying children and 97% were claimed by tax filers with qualifying children. Of this 97%, 36% were claimed by tax filers with one qualifying child, 40% were claimed by tax filers with two qualifying children, and 21% were claimed by tax filers with three or more qualifying children.

Though childless tax filers claimed 3% of all EITC dollars for 2014, they accounted for 26% of all tax filers that claimed the EITC. Thus, their small share of total EITC dollars reflects, in part, the lower credit amount available to childless filers.

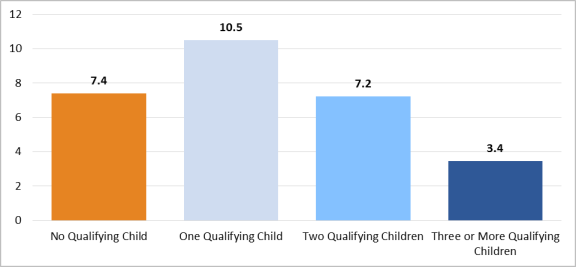

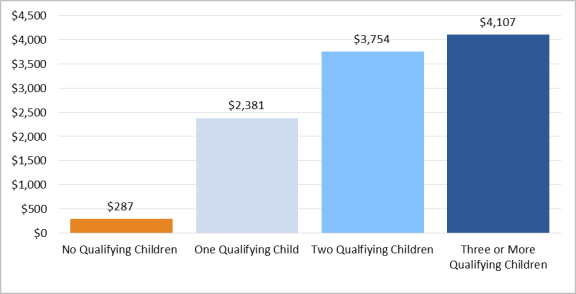

Figure 7 shows the number of returns claiming the EITC for 2014 by number of qualifying children. Figure 8 shows the average EITC claimed for 2014 by number of qualifying children. The average EITC for 2014 increased with the number of qualifying children a tax filer claimed:

- The EITC was claimed by 7.4 million tax filers with no qualifying children, with an average claim of $287.

- The EITC was claimed by 10.5 million filers with one qualifying child, with an average claim of $2,381.

- The EITC was claimed by 7.2 million filers with two qualifying children, with an average claim of $3,754.

- The EITC was claimed by 3.4 million filers with three or more qualifying children, with an average claim of $4,107.

|

Figure 7. Number of Tax Returns with EITC Claims for 2014, Number in Millions, Total Number of Returns Claiming the EITC = 28.5 million |

|

|

Source: Congressional Research Service, based on data from the U.S. Department of Treasury, Internal Revenue Services, SOI Tax Stats - Individual Income Tax Returns, Table 2.5. Notes: Detail does not add to total because of rounding. For detail on returns claiming the EITC by AGI and number of qualifying children, see Table A-2. |

|

Figure 8. Average EITC Claimed by Tax Filers in 2014 |

|

|

Source: Congressional Research Service, based on data from the U.S. Department of Treasury, Internal Revenue Services, SOI Tax Stats - Individual Income Tax Returns Publication 1304, Table 2.5. Note: For detail on returns claiming the EITC by AGI and number of qualifying children, see Table A-2. |

Income Level

Though the EITC is targeted toward lower-income earners, tax filers with children may receive the EITC even with income well above the poverty level. (The federal poverty level for a family of three was $20,420 in 2014.) However, the largest EITC benefits are focused on low-income earners near the poverty line, with those with greater earnings receiving reduced benefits.

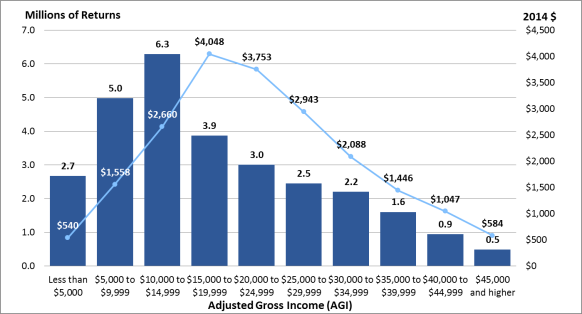

Figure 9 shows the number of tax returns with EITC claims for 2014 by adjusted gross income level. Figure 9 shows that the most typical (modal) EITC tax return had an AGI between $10,000 and $14,999, with 6.3 million returns including an EITC in that income range for 2014. For that year, close to half of all returns with EITC claims had AGIs below $15,000. This AGI is equivalent to earnings less than the $15,080 earned by a full-time (40 hour per week) full-year (52 weeks per year) worker earning the federal minimum wage ($7.25 per hour).

Figure 9 also shows the average EITC claimed by AGI category. Average EITC benefits first increase with AGI, then decline. This outcome reflects the formula for determining the EITC, which provides an increasing credit up to a maximum amount, then ultimately a reduced credit as it is phased out above a certain income threshold (see Table 1 and Figure 2). It also reflects a difference in the mix of family types claiming the EITC in the various AGI categories. For example, 71% of all filers claiming the EITC with AGIs of less than $5,000 had no qualifying children. All those claiming the EITC at AGIs above $20,000 in 2014 had qualifying children, and hence were eligible for a larger maximum EITC benefit than filers without children. For detail on returns claiming the EITC by AGI and number of qualifying children, see Table A-2.

|

Figure 9. Number of Returns Claiming the EITC and Average EITC Claimed for 2014, by Adjusted Gross Income Numbers in Millions and 2014 Dollars |

|

|

Source: Congressional Research Service, based on data from the U.S. Department of Treasury, Internal Revenue Services, SOI Tax Stats - Individual Income Tax Returns Table 2.5. Notes: For detail on returns claiming the EITC by AGI and number of qualifying children, see Table A-2. |

Filing and Marital Status

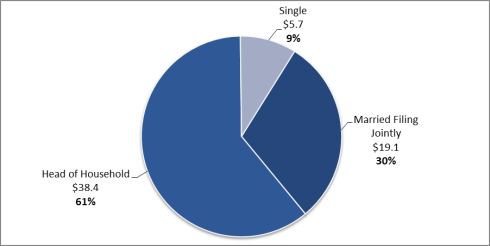

The Internal Revenue Service does not provide data on EITC dollars claimed by filing status. The Tax Policy Center (TPC), however, projects that in 2015, 70% of all EITC dollars will be claimed by unmarried tax filers (head of household and single filing statuses), with most (60% of all EITC dollars) claimed by those filing as heads of household. (The TPC projections are likely similar to the actual amounts of the EITC claimed by filing status in 2013 and 2014, given that they are based on the same credit formula.) Figure 10 shows projections for EITC dollars claimed by filing status for 2015.

|

Figure 10. Estimate of EITC Dollars Claimed by Marital Status, 2015 Dollars in Billions |

|

|

Source: Congressional Research Service, based on estimates from the Urban-Brookings Institution Tax Policy Center Table T13-0274, available at http://www.taxpolicycenter.org/numbers/index.cfm. Estimates are for tax year 2015. |

Region

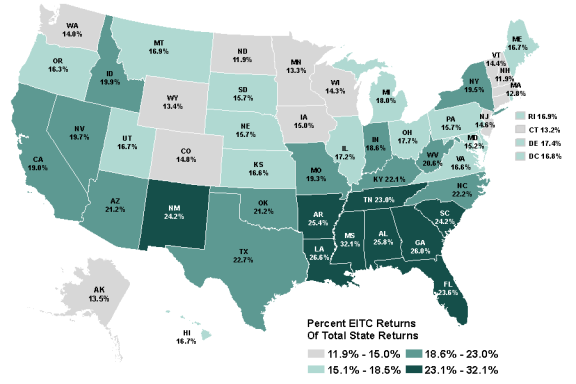

For tax year 2014, the EITC was claimed on 19.1% of all tax returns. However, the rate at which the EITC is claimed by tax filers varies considerably by state. In 2014, the state with the highest percentage of returns claiming the EITC was Mississippi, with the credit claimed on 32.1% of all returns. In contrast, the EITC was claimed on 11.9% of all returns in New Hampshire that year.

Figure 11 provides a map showing the percentage of all tax returns claiming the EITC by state. In addition to considerable state variation, the map shows that there is a regional pattern to EITC receipt. A greater share of returns filed in certain southern states claimed the EITC than returns in other regions of the country. The EITC was claimed on the smallest percentage of returns in New England as well as some states in the northern Midwest.

|

Figure 11. Percentage of Tax Returns Claiming the EITC by State for 2014 |

|

|

Source: Congressional Research Service, based on data from the U.S. Internal Revenue Service. Notes: For detail on EITC returns by state, see Table A-3. |

Appendix. Additional Tables

|

In millions of nominal dollars |

In millions of constant 2014 dollars |

||||||

|

Year |

Tax Filers Claiming the EITC (Millions) |

Total EITC |

Refunded EITC |

Average EITC |

Total EITC |

Refunded EITC |

Average EITC |

|

1975 |

6.215 |

1,250 |

900 |

201 |

5,500 |

3,960 |

884 |

|

1976 |

6.473 |

1,295 |

890 |

200 |

5,388 |

3,703 |

832 |

|

1977 |

5.627 |

1,127 |

880 |

200 |

4,403 |

3,438 |

781 |

|

1978 |

5.192 |

1,048 |

801 |

202 |

3,805 |

2,908 |

733 |

|

1979 |

7.135 |

2,052 |

1,395 |

288 |

6,691 |

4,549 |

939 |

|

1980 |

6.954 |

1,986 |

1,370 |

286 |

5,706 |

3,936 |

822 |

|

1981 |

6.717 |

1,912 |

1,278 |

285 |

4,980 |

3,328 |

742 |

|

1982 |

6.395 |

1,775 |

1,222 |

278 |

4,354 |

2,998 |

682 |

|

1983 |

7.368 |

1,795 |

1,289 |

244 |

4,266 |

3,064 |

580 |

|

1984 |

6.376 |

1,638 |

1,162 |

257 |

3,732 |

2,648 |

586 |

|

1985 |

7.432 |

2,088 |

1,499 |

281 |

4,594 |

3,298 |

618 |

|

1986 |

7.156 |

2,009 |

1,479 |

281 |

4,339 |

3,195 |

607 |

|

1987 |

8.738 |

3,391 |

2,930 |

388 |

7,067 |

6,106 |

809 |

|

1988 |

11.148 |

5,896 |

4,257 |

529 |

11,799 |

8,519 |

1,059 |

|

1989 |

11.696 |

6,595 |

4,636 |

564 |

12,591 |

8,851 |

1,077 |

|

1990 |

12.542 |

7,542 |

5,266 |

601 |

13,661 |

9,538 |

1,089 |

|

1991 |

13.665 |

11,105 |

8,183 |

813 |

19,302 |

14,223 |

1,413 |

|

1992 |

14.097 |

13,028 |

9,959 |

924 |

21,983 |

16,804 |

1,559 |

|

1993 |

15.117 |

15,537 |

12,028 |

1,028 |

25,454 |

19,706 |

1,684 |

|

1994 |

19.017 |

21,105 |

16,598 |

1,110 |

33,713 |

26,514 |

1,773 |

|

1995 |

19.334 |

25,956 |

20,829 |

1,343 |

40,320 |

32,355 |

2,086 |

|

1996 |

19.464 |

28,825 |

23,157 |

1,481 |

43,492 |

34,940 |

2,235 |

|

1997 |

19.391 |

30,389 |

24,396 |

1,567 |

44,823 |

35,984 |

2,311 |

|

1998 |

20.273 |

32,340 |

27,175 |

1,595 |

46,970 |

39,468 |

2,317 |

|

1999 |

19.259 |

31,901 |

27,604 |

1,656 |

45,331 |

39,225 |

2,353 |

|

2000 |

19.277 |

32,296 |

27,803 |

1,675 |

44,400 |

38,223 |

2,303 |

|

2001 |

19.593 |

35,784 |

29,043 |

1,826 |

47,834 |

38,823 |

2,441 |

|

2002 |

21.574 |

37,786 |

33,258 |

1,751 |

49,724 |

43,765 |

2,304 |

|

2003 |

22.112 |

39,186 |

34,508 |

1,772 |

50,417 |

44,398 |

2,280 |

|

2004 |

22.270 |

40,024 |

35,299 |

1,797 |

50,159 |

44,238 |

2,252 |

|

2005 |

22.752 |

42,410 |

37,465 |

1,864 |

51,408 |

45,414 |

2,259 |

|

2006 |

23.042 |

44,388 |

39,072 |

1,926 |

52,124 |

45,882 |

2,262 |

|

2007 |

24.584 |

48,540 |

42,508 |

1,974 |

55,421 |

48,534 |

2,254 |

|

2008 |

24.756 |

50,669 |

44,260 |

2,047 |

55,713 |

48,666 |

2,251 |

|

2009 |

27.041 |

59,240 |

53,985 |

2,191 |

65,370 |

59,571 |

2,418 |

|

2010 |

27.368 |

59,562 |

54,256 |

2,176 |

64,664 |

58,904 |

2,362 |

|

2011 |

27.912 |

62,906 |

55,350 |

2,254 |

66,205 |

58,253 |

2,372 |

|

2012 |

27.848 |

64,129 |

56,190 |

2,303 |

66,124 |

57,938 |

2,375 |

|

2013 |

28.822 |

68,084 |

59,145 |

2,362 |

69,189 |

60,104 |

2,400 |

|

2014 |

28.538 |

68,339 |

58,889 |

2,395 |

68,339 |

58,889 |

2,395 |

Source: Congressional Research Service. For pre-2003 data, U.S. Congress, House Committee on Ways and Means, 2004 Green Book, Background Material and Data on Programs Within the Jurisdiction of the Committee on Ways and Means, 108th Congress, 2nd session, WMCP 108-6, March 2004, pp. 13-41. For 2003 and later data, Internal Revenue Service, Total File, United States, Individual Income and Tax Data, by State and Size of Adjusted Gross Income, 2003 through 2014, expanded unpublished version, Table 2.5.

Note: Constant 2014 dollars were computed using the Consumer Price Index for all Urban Consumers (CPI-U).

Table A-2. Average EITC, Number of Returns with EITC Claimed, and Total EITC Benefits for 2014, by Adjusted Gross Income

|

AGI |

Totals |

No Qualifying Children |

One Qualifying Child |

Two Qualifying Children |

Three or More Qualifying Children |

|

Average Credit |

|||||

|

Less than $5,000 |

$540 |

$215 |

$1,162 |

$1,562 |

$1,810 |

|

$5,000 to $9,999 |

1,558 |

427 |

2,787 |

3,072 |

3,503 |

|

$10,000 to $14,999 |

2,660 |

202 |

3,254 |

5,028 |

5,648 |

|

$15,000 to $19,999 |

4,048 |

183 |

3,199 |

5,315 |

5,985 |

|

$20,000 to $24,999 |

3,753 |

0 |

2,644 |

4,687 |

5,501 |

|

$25,000 to $29,999 |

2,943 |

0 |

1,934 |

3,731 |

4,551 |

|

$30,000 to $34,999 |

2,088 |

0 |

1,157 |

2,728 |

3,549 |

|

$35,000 to $39,999 |

1,446 |

0 |

565 |

1,821 |

2,611 |

|

$40,000 to $44,999 |

1,047 |

0 |

323 |

925 |

1,694 |

|

$45,000 and higher |

584 |

0 |

0 |

418 |

717 |

|

Totals |

2,395 |

287 |

2,381 |

3,754 |

4,107 |

|

Total Returns with EITC |

|||||

|

Less than $5,000 |

2,678,792 |

1,901,415 |

491,682 |

201,590 |

84,107 |

|

$5,000 to $9,999 |

4,980,767 |

2,708,132 |

1,600,850 |

487,921 |

183,865 |

|

$10,000 to $14,999 |

6,293,185 |

2,452,653 |

1,915,924 |

1,391,897 |

532,710 |

|

$15,000 to $19,999 |

3,871,549 |

321,082 |

1,712,112 |

1,291,965 |

546,390 |

|

$20,000 to $24,999 |

3,008,698 |

0 |

1,553,646 |

1,000,063 |

453,989 |

|

$25,000 to $29,999 |

2,454,246 |

0 |

1,253,596 |

811,158 |

389,492 |

|

$30,000 to $34,999 |

2,203,407 |

0 |

1,078,788 |

777,014 |

347,605 |

|

$35,000 to $39,999 |

1,609,000 |

0 |

692,988 |

577,388 |

338,624 |

|

$40,000 to $44,999 |

945,503 |

0 |

191,427 |

454,086 |

299,990 |

|

$45,000 and higher |

492,762 |

0 |

0 |

220,167 |

272,595 |

|

Totals |

28,537,909 |

7,384,282 |

10,491,013 |

7,213,249 |

3,449,367 |

|

Total EITC Claimed ($ in Thousands) |

|||||

|

Less than $5,000 |

1,447,759 |

409,156 |

571,509 |

314,839 |

152,256 |

|

$5,000 to $9,999 |

7,760,435 |

1,156,586 |

4,460,893 |

1,498,859 |

644,096 |

|

$10,000 to $14,999 |

16,736,984 |

496,528 |

6,233,653 |

6,997,885 |

3,008,917 |

|

$15,000 to $19,999 |

15,672,521 |

58,671 |

5,477,335 |

6,866,382 |

3,270,132 |

|

$20,000 to $24,999 |

11,291,513 |

1 |

4,107,069 |

4,687,078 |

2,497,366 |

|

$25,000 to $29,999 |

7,223,624 |

0 |

2,424,338 |

3,026,636 |

1,772,650 |

|

$30,000 to $34,999 |

4,601,608 |

0 |

1,248,334 |

2,119,707 |

1,233,567 |

|

$35,000 to $39,999 |

2,327,289 |

0 |

391,534 |

1,051,649 |

884,106 |

|

$40,000 to $44,999 |

989,895 |

0 |

61,764 |

420,006 |

508,126 |

|

$45,000 and higher |

287,554 |

0 |

0 |

91,987 |

195,567 |

|

Totals |

68,339,182 |

2,120,942 |

24,976,429 |

27,075,028 |

14,166,783 |

Source: Congressional Research Service, based on data from the U.S. Department of the Treasury, Internal Revenue Services, SOI Tax Stats - Individual Income Tax Returns Publication 1304, Table 2.5.

|

State or Area |

Total Returns |

Returns with EITC Claimed |

Percentage of Total Returns with EITC Claimed |

Total EITC Claimed (In thousands $) |

Average EITC |

Percent of EITC Refunded |

|

United States total |

147,766,770 |

28,233,280 |

19.1% |

$67,720,175 |

$2,399 |

86.4% |

|

Alabama |

2,046,560 |

529,020 |

25.8 |

1,444,910 |

2,731 |

89.0 |

|

Alaska |

361,130 |

48,620 |

13.5 |

98,599 |

2,028 |

88.9 |

|

Arkansas |

1,223,140 |

310,300 |

25.4 |

794,507 |

2,560 |

88.4 |

|

Arizona |

2,845,710 |

603,080 |

21.2 |

1,522,532 |

2,525 |

87.6 |

|

California |

17,411,400 |

3,312,640 |

19.0 |

7,748,313 |

2,339 |

83.2 |

|

Colorado |

2,553,250 |

377,440 |

14.8 |

810,024 |

2,146 |

86.1 |

|

Connecticut |

1,749,470 |

231,640 |

13.2 |

497,420 |

2,147 |

86.5 |

|

Delaware |

443,820 |

77,250 |

17.4 |

178,189 |

2,307 |

90.3 |

|

District of Columbia |

336,950 |

56,590 |

16.8 |

129,888 |

2,295 |

86.8 |

|

Florida |

9,398,920 |

2,218,780 |

23.6 |

5,404,377 |

2,436 |

84.7 |

|

Georgia |

4,378,120 |

1,138,570 |

26.0 |

3,063,653 |

2,691 |

86.4 |

|

Hawaii |

681,840 |

114,020 |

16.7 |

246,619 |

2,163 |

89.0 |

|

Idaho |

701,990 |

139,650 |

19.9 |

317,425 |

2,273 |

87.2 |

|

Illinois |

6,131,110 |

1,055,660 |

17.2 |

2,582,429 |

2,446 |

85.6 |

|

Indiana |

3,078,750 |

571,260 |

18.6 |

1,348,571 |

2,361 |

88.6 |

|

Iowa |

1,445,570 |

216,720 |

15.0 |

476,999 |

2,201 |

88.4 |

|

Kansas |

1,336,440 |

221,190 |

16.6 |

511,361 |

2,312 |

89.3 |

|

Kentucky |

1,891,820 |

418,880 |

22.1 |

986,209 |

2,354 |

88.2 |

|

Louisiana |

2,007,830 |

533,130 |

26.6 |

1,461,088 |

2,741 |

88.1 |

|

Maine |

638,280 |

106,820 |

16.7 |

217,211 |

2,033 |

85.4 |

|

Maryland |

2,935,560 |

445,690 |

15.2 |

1,017,496 |

2,283 |

84.9 |

|

Massachusetts |

3,343,720 |

427,330 |

12.8 |

873,980 |

2,045 |

87.3 |

|

Michigan |

4,685,320 |

844,910 |

18.0 |

2,031,147 |

2,404 |

86.3 |

|

Minnesota |

2,687,780 |

357,410 |

13.3 |

761,404 |

2,130 |

87.6 |

|

Mississippi |

1,243,420 |

399,570 |

32.1 |

1,128,094 |

2,823 |

88.8 |

|

Missouri |

2,767,370 |

535,370 |

19.3 |

1,266,203 |

2,365 |

88.6 |

|

Montana |

492,010 |

83,200 |

16.9 |

172,795 |

2,077 |

87.3 |

|

Nebraska |

889,100 |

139,700 |

15.7 |

319,361 |

2,286 |

88.6 |

|

Nevada |

1,321,700 |

260,620 |

19.7 |

622,817 |

2,390 |

87.4 |

|

New Hampshire |

685,010 |

81,730 |

11.9 |

157,544 |

1,928 |

85.5 |

|

New Jersey |

4,342,620 |

633,940 |

14.6 |

1,444,010 |

2,278 |

84.9 |

|

New Mexico |

911,750 |

220,440 |

24.2 |

529,254 |

2,401 |

89.8 |

|

New York |

9,523,840 |

1,857,050 |

19.5 |

4,273,027 |

2,301 |

83.9 |

|

North Carolina |

4,380,810 |

974,660 |

22.2 |

2,382,346 |

2,444 |

87.7 |

|

North Dakota |

370,570 |

44,180 |

11.9 |

91,023 |

2,060 |

88.3 |

|

Ohio |

5,559,950 |

986,380 |

17.7 |

2,339,276 |

2,372 |

88.3 |

|

Oklahoma |

1,639,860 |

348,000 |

21.2 |

853,551 |

2,453 |

87.8 |

|

Oregon |

1,826,550 |

297,650 |

16.3 |

616,801 |

2,072 |

87.6 |

|

Pennsylvania |

6,169,090 |

969,860 |

15.7 |

2,134,260 |

2,201 |

88.7 |

|

Rhode Island |

521,890 |

88,070 |

16.9 |

197,398 |

2,241 |

87.8 |

|

South Carolina |

2,124,300 |

513,350 |

24.2 |

1,282,656 |

2,499 |

88.6 |

|

South Dakota |

410,920 |

64,620 |

15.7 |

140,406 |

2,173 |

89.5 |

|

Tennessee |

2,928,360 |

674,840 |

23.0 |

1,683,788 |

2,495 |

86.6 |

|

Texas |

11,992,010 |

2,720,390 |

22.7 |

7,188,558 |

2,642 |

85.3 |

|

Utah |

1,221,670 |

204,370 |

16.7 |

471,171 |

2,305 |

88.1 |

|

Vermont |

322,860 |

46,420 |

14.4 |

87,885 |

1,893 |

84.5 |

|

Virginia |

3,871,680 |

641,360 |

16.6 |

1,457,910 |

2,273 |

87.5 |

|

Washington |

3,342,750 |

466,800 |

14.0 |

994,273 |

2,130 |

88.0 |

|

West Virginia |

782,960 |

161,330 |

20.6 |

357,972 |

2,219 |

90.6 |

|

Wisconsin |

2,811,290 |

401,440 |

14.3 |

873,359 |

2,176 |

88.5 |

|

Wyoming |

279,930 |

37,520 |

13.4 |

77,435 |

2,064 |

89.0 |

|

Other Areas |

718,040 |

23,850 |

3.3 |

52,651 |

2,208 |

96.2 |

Source: Congressional Research Service, based on data from the U.S. Department of the Treasury, Internal Revenue Service (IRS), Individual Income and Tax Data, by State and Size of Adjusted Gross Income.

Note: Totals in this table differ slightly from total shown in Table A-2. While the figures in Table A-2 and Table A-3 are both based on data from the IRS, the data in Table A-3 include "substitutes for returns" in which the IRS constructs tax returns for certain nonfilers.